Three Key Findings Shed New Light on Fundraising in 2020

Aumni and the National Venture Capital Association (NVCA) recently hosted a webinar on the latest major updates to the Enhanced Model Term Sheet. The Enhanced Model Term Sheet has enabled investors to draft term sheets while comparing terms against market benchmarks. Aumni's AI-driven technology has been powering these insights based on anonymized venture financing data extracted from more than 100,000 venture transactions, representing 40,000 investors with a combined network of over $1 trillion in assets under management (AUM) – the largest aggregate analysis of private venture deal term data conducted to date.

The partnership between Aumni and NVCA was launched in July 2020 and has been met with overwhelmingly positive reviews. Over 83% of customers cited the term sheet as “very useful.” Since its initial offering, there have been over 3,000 downloads by investors (VCs, LPs, Angel), law firms, companies, and founders. The top use cases so far have included customers who have:

- Benchmarked past deals with market performance

- Standardized future deals for efficiency

- Identified trends to adopt

The latest version boasts thirteen additional term analytics as well as the ability to compare last year’s data with historical data. Here are some of the 2020 insights Aumni has gathered:

Insight #1 - 2020 was good for companies

Despite the uncertainty experienced during the pandemic, last year was good for companies. Aumni has collected data to help illustrate this phenomenon. As companies enjoyed a median increase in the amount of capital raised at every stage, investors acted with confidence. With round sizes up, post-money company valuation is also rising.

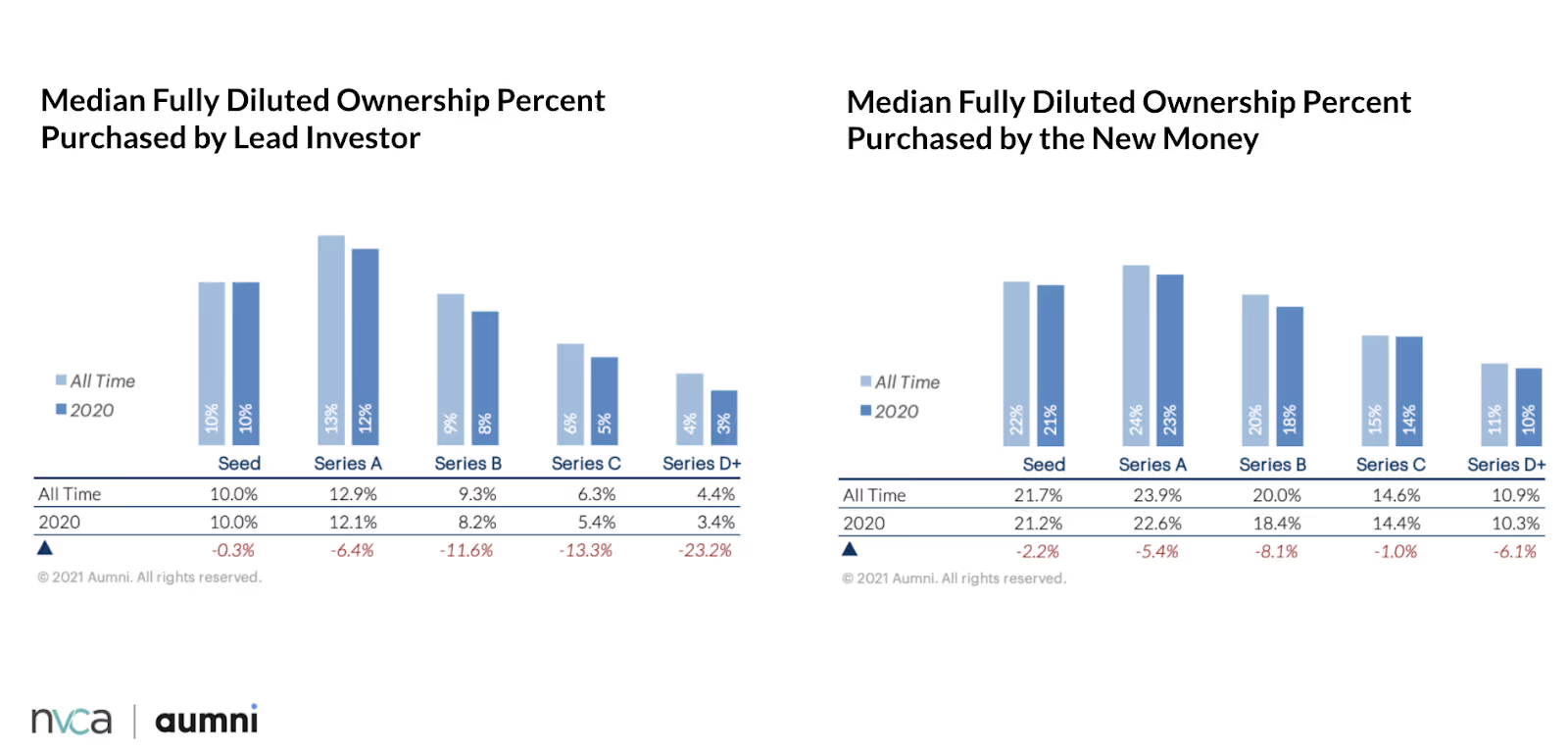

Dilution levels also favored companies in 2020. At the median, lead investors are owning less of the company than they have historically, leaving a higher percentage of ownership in the hands of the founders. This data is showing the total amount of new equity capital that's being raised and the fully diluted ownership percentage of that class. The chart on the right reinforces those findings but speaks to the way new money is invested across the total class of shares, by round.

These small deviations in percentage confirm the trend that good companies receive funding on great terms, and they're retaining greater ownership of their company in later rounds than they have historically.

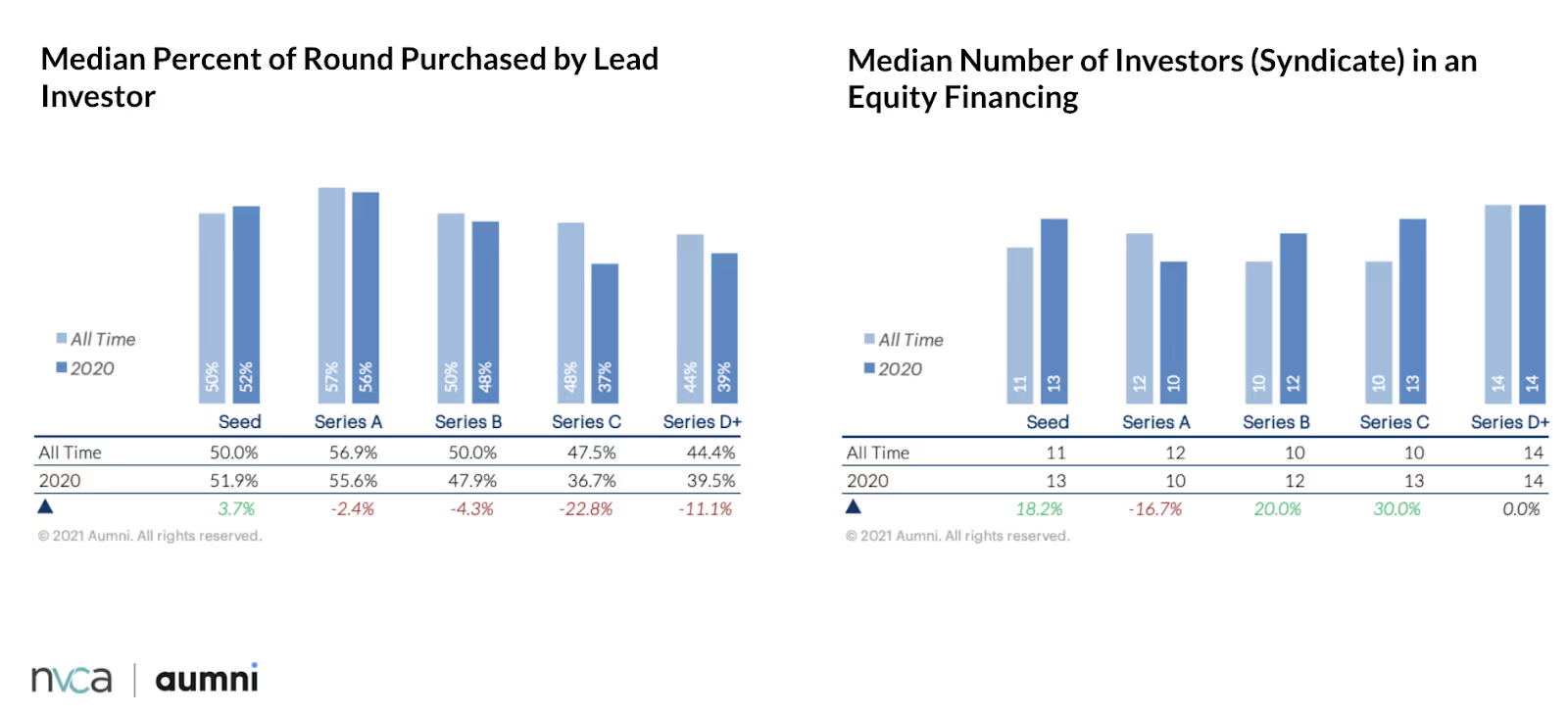

Insight #2- Capital raising dynamics are evolving

Venture and capital raising dynamics are changing. Aumni’s team has seen activity among firms trying to build broad syndicates, along with the desire to be particularly strategic about what type of ownership percentages they are taking. The discovery of data-driven insight provides a clear understanding of the market and how deals are forming, which in turn, may inform negotiation tactics.

Headlines in the venture world highlight the amount of capital raised and the valuation of a company. But that's only one aspect of the conversation between founders and investors. Evaluating fund dynamics, ownership targets, and normal dilution are all best practices. Access to accurate data benchmarking allows a more fruitful negotiation and aligns the interests between lead investors, other investors in the companies, and the founders. Be aware that the round structure and dynamics of venture financings are also changing, bolstered by the proliferation of emerging managers with capital to deploy at the venture stage.

One interesting data point here is the median percent of the round purchased by the lead investor. Historically, a lead investor would typically take half of the round. What we can see are slight changes across the various rounds, especially following the seed round. Lead investors are taking a smaller percentage of the total allocation than taken in previous years.

What causes this shift? Several factors apply but, generally, an abundance of providers are in-market with a healthy supply of capital, conditions that yield opportunities for companies to stitch together syndicates and create new possibilities for allocation. Pro-rata dynamics are playing into this shift as well. Seed and Series A funds typically maintain rights to purchase and maintain allocations in future rounds. We're seeing earlier-stage funds stepping up and investing in later-stage rounds. There are various ways that they can do that through their fund dynamics. Overall, we have seen the dynamics evolve for both emerging and larger funds, inviting them to diversify and consider new ownership strategies.

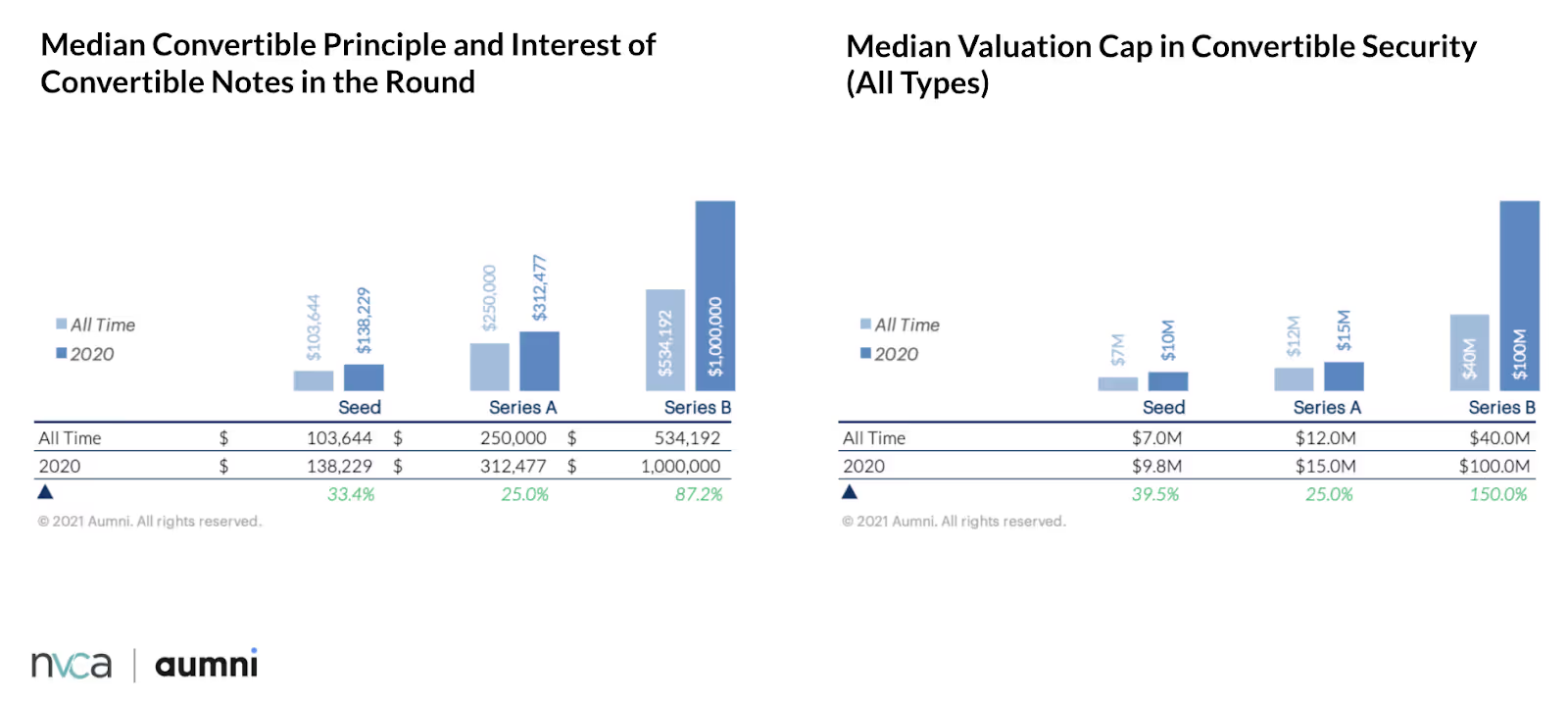

#3 - Early-stage venture is flourishing

The earliest stages of venture investing are growing in popularity. This next dataset speaks to entrepreneurs, angel investors, and investors that are seeking to fund innovation at the earliest stages of a company. Last year, we saw an increase in the median convertible at the seed round. This trend is continuing in terms of the median value. For entrepreneurs looking to strike while the market is hot, this is an opportune time to leverage your problem-solving idea to create a company. This is an exciting trend for innovation overall, as we are seeing more capital deployed earlier.

Market benchmarks on convertible vehicles are difficult to access. Yet, access to this data creates clarity for companies and investors alike, especially as it is conventional for early-stage investments to take the form of convertible notes, SAFEs, etc. Even early-stage companies can negotiate higher valuation caps than what was historically possible. Reliable data that is available to us today can reduce friction, aligning investors and founders who desire greater transparency into potential outcomes.

In partnership with the NVCA, Aumni is discovering valuable new insight previously locked in the data we’ve gathered from previously private executed term sheets. Our unique access, aggregation, and reporting shed light on these terms and their impact on the financial outcomes sought by funds, founders, and limited partners. Meaningful answers are found in the market term sheet benchmarks and we invite you to explore.

.avif)

©2025 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC.

This material is not the product of J.P. Morgan’s Research Department. It is not a research report and is not intended as such. This material is provided for informational purposes only and is subject to change without notice. It is not intended as research, a recommendation, advice, offer or solicitation to buy or sell any financial product or service, or to be used in any way for evaluating the merits of participating in any transaction. Please consult your own advisors regarding legal, tax, accounting or any other aspects including suitability implications, for your particular circumstances or transactions. J.P. Morgan and its third-party suppliers disclaim any responsibility or liability whatsoever for the quality, fitness for a particular purpose, non-infringement, accuracy, currency or completeness of the information herein, and for any reliance on, or use of this material in any way. Any information or analysis in this material purporting to convey, summarize, or otherwise rely on data may be based on a sample or normalized set thereof. This material is provided on a confidential basis and may not be reproduced, redistributed or transmitted, in whole or in part, without the prior written consent of J.P. Morgan. Any unauthorized use is strictly prohibited. Any product names, company names and logos mentioned or included herein are trademarks or registered trademarks of their respective owners.

Aumni, Inc. (“Aumni”) is a wholly-owned subsidiary of JPMorgan Chase & Co. Access to the Aumni platform is subject to execution of an applicable platform agreement and order form and access will be granted by J.P. Morgan in its sole discretion. J.P. Morgan is the global brand name for JPMorgan Chase & Co. and its subsidiaries and affiliates worldwide. Aumni does not provide any accounting, regulatory, tax, insurance, investment, or legal advice. The recipient of any information provided by Aumni must make an independent assessment of any legal, credit, tax, insurance, regulatory and accounting issues with its own professional advisors in the context of its particular circumstances. Aumni is neither a broker-dealer nor a member of any exchanges or self-regulatory organizations.

383 Madison Ave, New York, NY 10017