How technology drives cost savings and improves audits for venture firms

.avif)

Efficiency is key when it comes to managing audits, especially since overages and delays can lead to increased direct and indirect costs. As firms grow and portfolios expand, the complexity of audit processes can become overwhelming. Traditional methods reliant on manual data entry and paper trails are no longer sufficient to meet the demands of today’s market.

Leveraging technology and data is now a necessity for streamlining audit processes, leading to cost savings and improved outcomes for venture teams. Below, we detail four key steps venture teams can take to enable a more data-driven, tech-enabled financial audit.

1. Improve audit readiness with data-driven insights into portfolio activity

Preparation is essential for reducing friction during the audit cycle. As outlined in Aumni’s Audit Preparation Checklist, funds can take steps in advance, including screening the portfolio for new investments, stale valuations, and complex situations; collecting key deal docs; and gathering financial performance and the latest cap table from select portfolio companies.

- Screen the portfolio ahead of audit kick-off: Technology in modern platforms enables fund managers to screen their portfolios based on key attributes such as Last Equity Financing Date, Stage, and Fund Cost. These attributes can help funds quickly find new investments across the financial period, identify potentially stale valuations (12+ months since a financing), and flag complex situations (large positions or late-stage companies).

- Collect key deal docs: Based on new purchases and sales across the years, fund managers can ensure they have all the necessary deal docs that auditors are likely to ask for. Storing these documents in a technology platform with LLM-powered hyperlinking to key terms helps funds quickly surface key legal terms auditors may request.

- Gather financial performance and cap tables: Leveraging technology to automatically request or structure financial performance information from portfolio companies enables fund managers and auditors to quickly identify holdings that may require a deeper look, avoiding surprises.

Having these materials organized ahead of time can shorten timelines and reduce the need for extensive back-and-forth with auditors.

2. Use technology to quickly respond to auditor inquiries

Modern platforms have created opportunities for funds to centralize and structure data from core documents. The most effective tools enable finance teams and their auditors to access investment terms, legal structures, and ownership information in one place, minimizing manual review and version control issues.

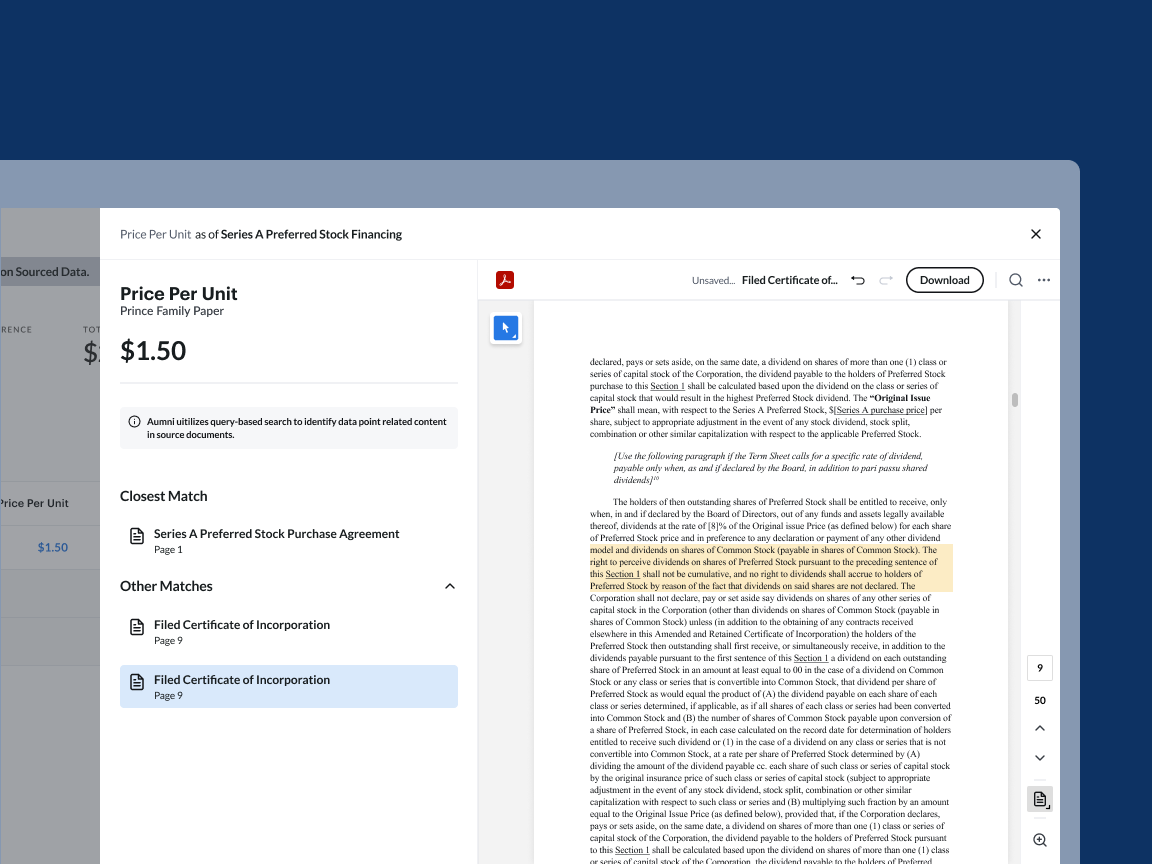

- LLM-assisted hyperlinking to key terms: Some of the most commonly validated data points relate to legal and economic rights that the investor has that could impact fair value, including liquidation preference, conversion multiples, seniority, and original issue price. LLM-assisted hyperlinking enables fund managers and auditors to quickly navigate to these key terms in legal documents.

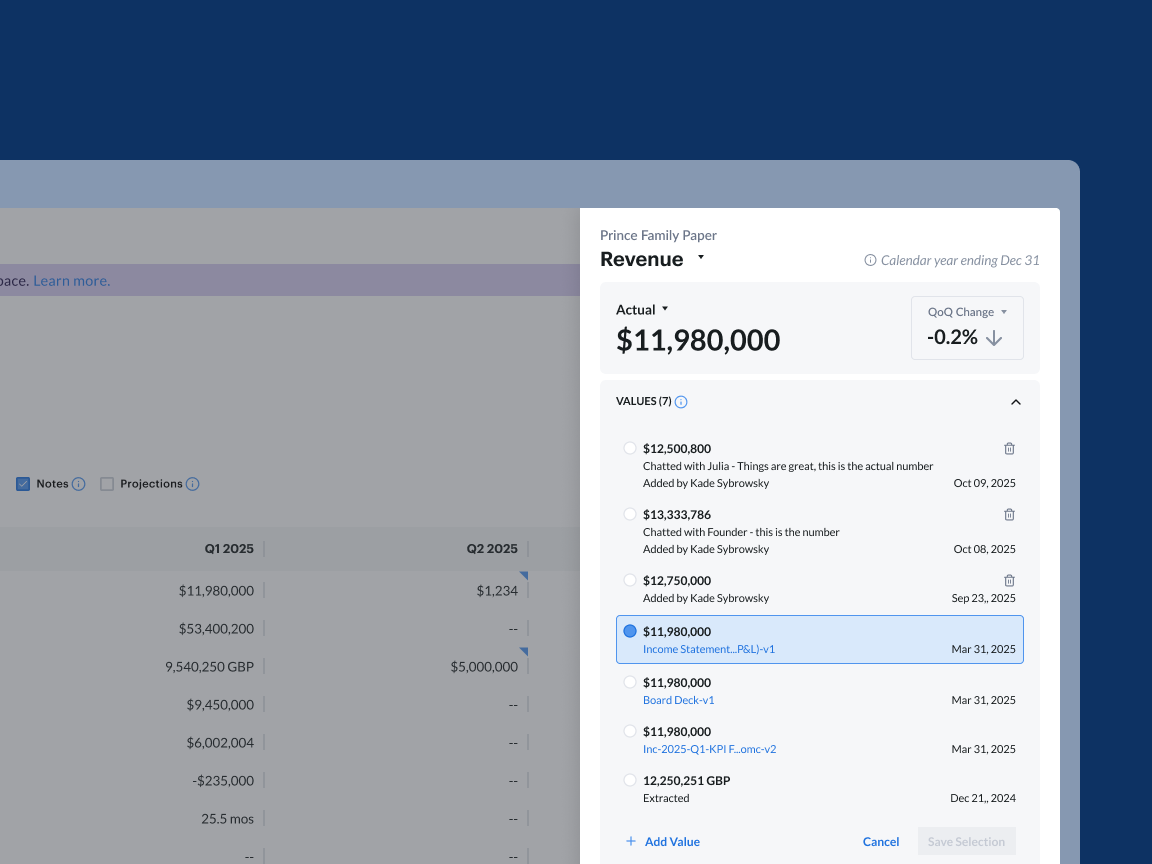

- Integration of data sources: Integrating disparate data sources into a centralized platform provides a single source of truth. For example, portfolio company capitalization could be found in both the share purchase agreement and the cap table—so which one should take precedent? Or the financial statements say ARR is $5M, but the board deck says $4.5M—which is the figure to use and why? Seamless integration enables reconciliation and validation of multiple data sources, and an activity log to enable simple verification of changes.

3. Provide auditors with direct access to portfolio management software for self-service

Section 32’s COO & CFO, Nina Labatt, noted that providing auditors with limited, read-only access to Aumni allowed them to independently verify key terms and reduce time spent on routine questions. This level of transparency also helped auditors contextualize transactions and assess valuation assumptions earlier in the process.

You can listen to the full conversation with Nina Labatt here.

Direct access to structured data and legal terms fundamentally changes the audit experience. Instead of sifting through endless email threads or waiting on document requests, auditors can quickly locate and review the information they need. Immediate access streamlines the validation process, allowing auditors to independently verify ownership, economic rights, and cap table data—without the risk of miscommunication that often comes with manual exchanges.

Detailed activity logs can also enhance transparency, making it easier to track every change and update, essentially providing a clear audit trail and supporting compliance requirements. These capabilities do more than just save time; they foster a more efficient collaborative, and trustworthy audit cycle, benefiting both the firm and its stakeholders.

4. Run valuation exercises and scenarios to support fair value determinations

For private funds, modeling hypothetical exit scenarios is a practical way to assess potential future value and strengthen the credibility of fair value determinations. Exit waterfalls—frameworks that dictate how proceeds are distributed in an exit—are central to this process, ensuring all stakeholders are compensated according to the deal’s terms.

An exit waterfall lays out the order and priority of payments when a company is sold or liquidates, covering key terms like liquidation preference, participation rights, seniority, conversion ratios, cumulative dividends, warrants, options, and anti-dilution clauses.

Download Aumni’s Venture Portfolio Company Exit Waterfall Guide here.

Technology now enables funds to automate much of this analysis. By extracting and structuring data from venture transactions and legal agreements, finance teams can efficiently run scenario-based tests, calibrate fair value models, and ensure their exit strategies are aligned with market standards.

But exit waterfalls are just one piece of the puzzle. Comprehensive valuation exercises should also incorporate the three primary methodologies:

- Market approach: Values the company based on comparable transactions and public market data, adjusted for risk and growth differences.

- Income approach: Estimates value using the present value of expected future cash flows, often through discounted cash flow (DCF) analysis.

- Asset approach: Assesses value based on the fair value of a company’s assets and liabilities—useful as a reality check or for early-stage, asset-heavy businesses.

Why a tech-enabled audit process matters

Bringing technology and data into the audit process isn’t just about speed—it’s about clarity, transparency, and confidence. When finance teams and auditors have direct access to structured data, automated workflows, and real-time insights, audits become less of a burden and more of a strategic advantage.

The result? Fewer surprises, faster turnaround, and a stronger foundation for decision-making and compliance. As more venture firms embrace these tools, the audit process is evolving from a manual, reactive exercise to a proactive, value-adding function.

Ready to simplify your next audit? Explore document management.

Read next: How Floodgate saved 20+ hours in audit prep using Aumni

.avif)

.avif)

.avif)

©2025 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC.

This material is not the product of J.P. Morgan’s Research Department. It is not a research report and is not intended as such. This material is provided for informational purposes only and is subject to change without notice. It is not intended as research, a recommendation, advice, offer or solicitation to buy or sell any financial product or service, or to be used in any way for evaluating the merits of participating in any transaction. Please consult your own advisors regarding legal, tax, accounting or any other aspects including suitability implications, for your particular circumstances or transactions. J.P. Morgan and its third-party suppliers disclaim any responsibility or liability whatsoever for the quality, fitness for a particular purpose, non-infringement, accuracy, currency or completeness of the information herein, and for any reliance on, or use of this material in any way. Any information or analysis in this material purporting to convey, summarize, or otherwise rely on data may be based on a sample or normalized set thereof. This material is provided on a confidential basis and may not be reproduced, redistributed or transmitted, in whole or in part, without the prior written consent of J.P. Morgan. Any unauthorized use is strictly prohibited. Any product names, company names and logos mentioned or included herein are trademarks or registered trademarks of their respective owners.

Aumni, Inc. (“Aumni”) is a wholly-owned subsidiary of JPMorgan Chase & Co. Access to the Aumni platform is subject to execution of an applicable platform agreement and order form and access will be granted by J.P. Morgan in its sole discretion. J.P. Morgan is the global brand name for JPMorgan Chase & Co. and its subsidiaries and affiliates worldwide. Aumni does not provide any accounting, regulatory, tax, insurance, investment, or legal advice. The recipient of any information provided by Aumni must make an independent assessment of any legal, credit, tax, insurance, regulatory and accounting issues with its own professional advisors in the context of its particular circumstances. Aumni is neither a broker-dealer nor a member of any exchanges or self-regulatory organizations.

383 Madison Ave, New York, NY 10017