Are investors passing on pari passu?

.avif)

What might the prevalence of pari passu deal structures in startup fundraising indicate about market dynamics?

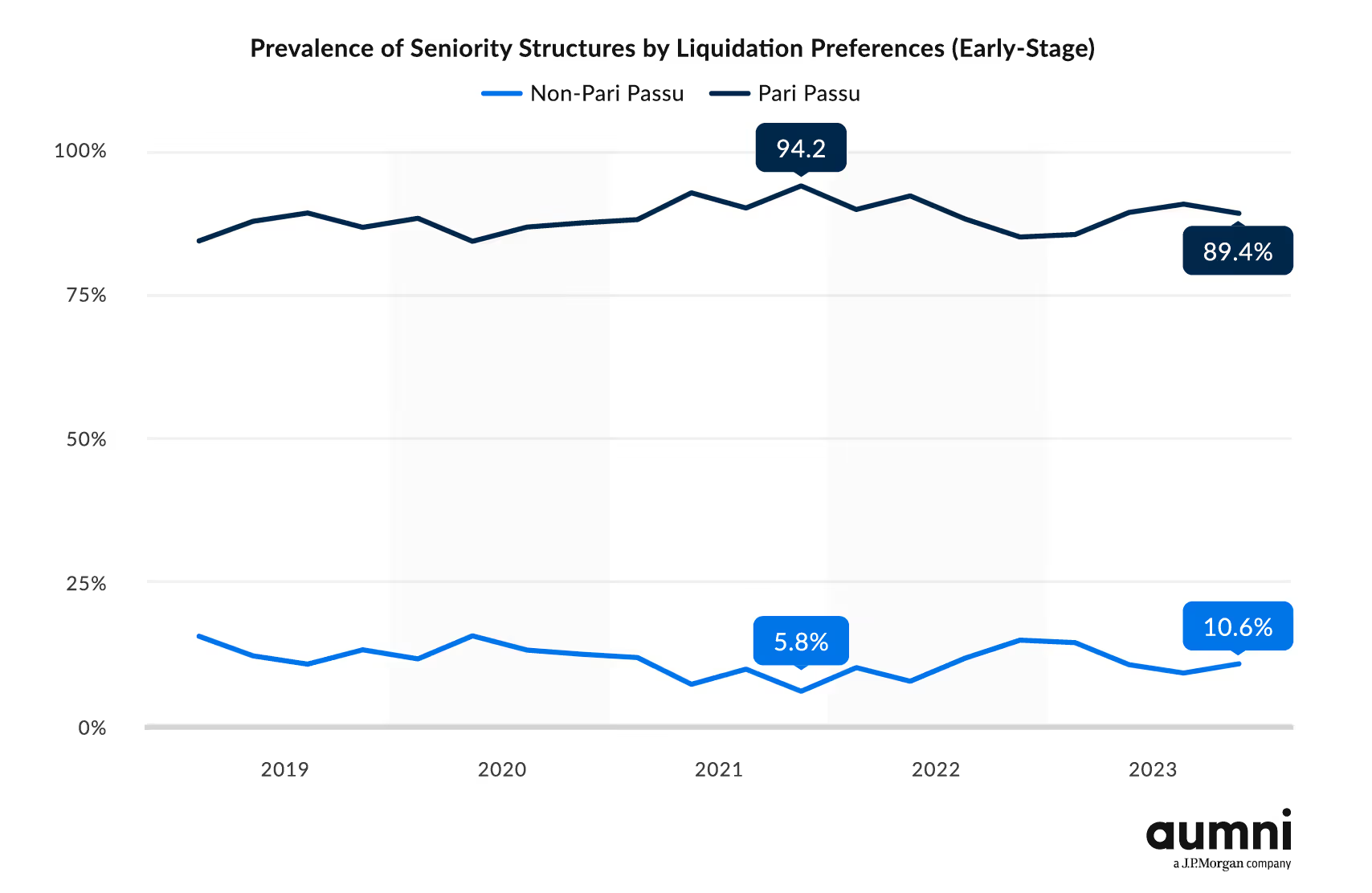

The percentage of transactions issuing shares pari passu peaked along with the venture market in 2021. However, in 2022, as deal volume dropped, the percentage of deals with more structure began increasing.

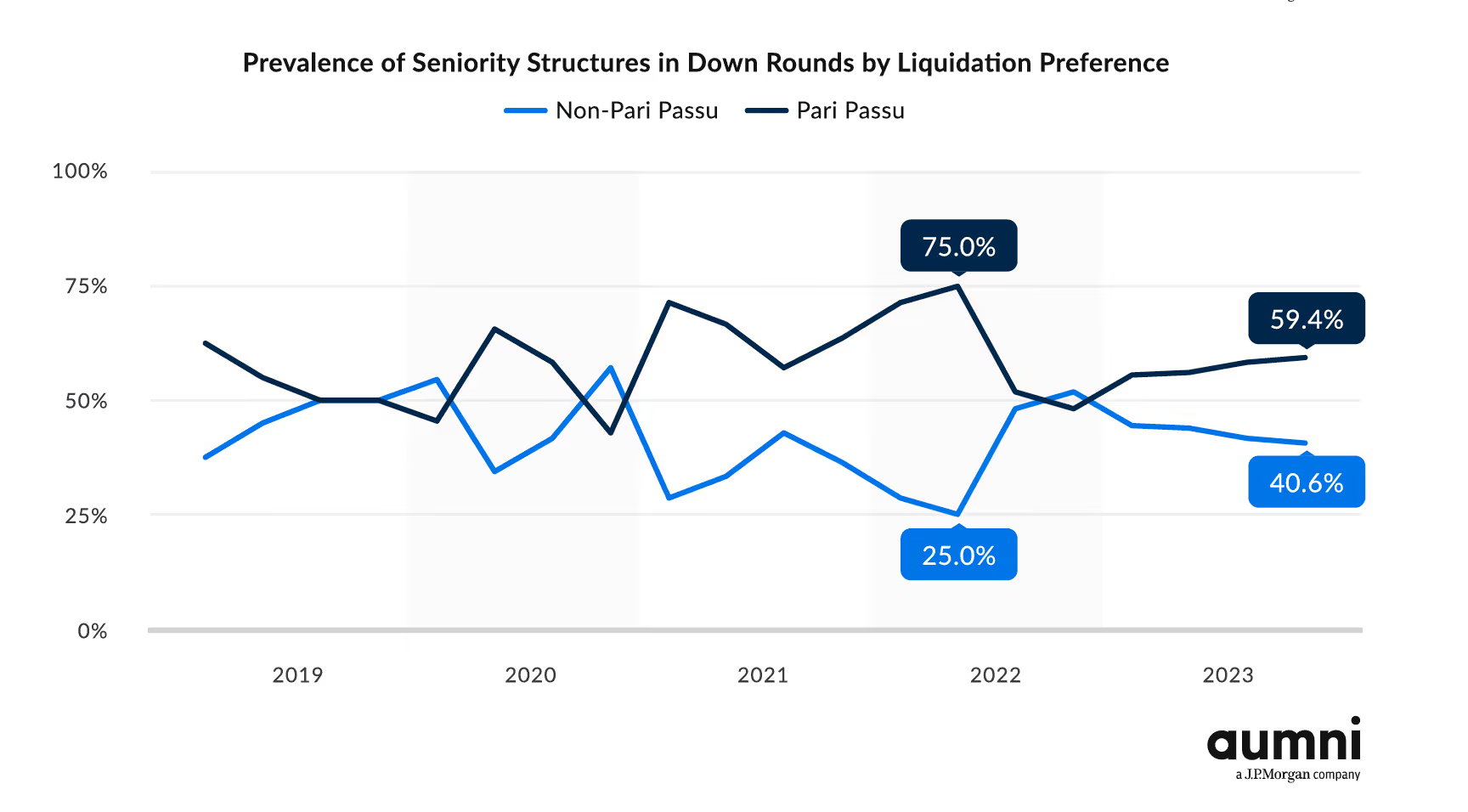

For background, pari passu deal structures bring new investors onto the cap table on “equal footing” (i.e. the same level of seniority) as other previous investors. In contrast, creating a seniority structure among the equity holders would preference (usually more recent) investors who purchased shares that are more senior in the capital structure (i.e. get made whole first in the event of a liquidation). In terms of sentiment, pari passu is generally considered to be a relatively neutral set of terms while other more structured terms, such as seniority ordered-by-equity-class (sometimes known as “standard” structure), tend to be thought of as investor‑friendly.

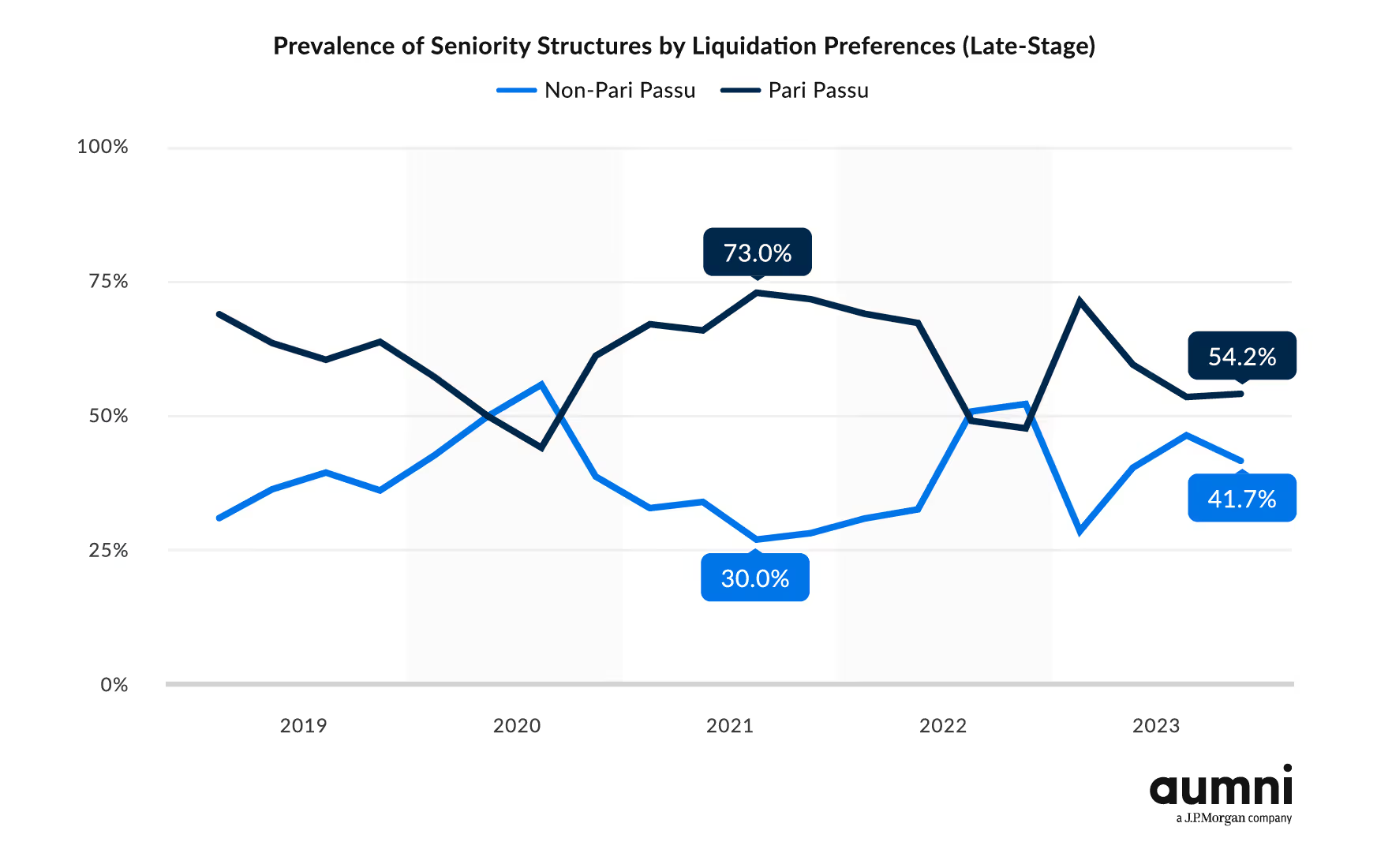

Above, we charted the frequency of pari passu in startup deal terms against ordered-by-equity class and bespoke structures (“non-pari passu”). According to data from Aumni-tracked venture deals, a notable shift started in 2021, with an uptick in the number of transactions completed non-pari passu. This trend is most apparent in late-stage deals, where the prevalence of pari passu has fallen by ~20 percentage points from the 2021 peak to today.

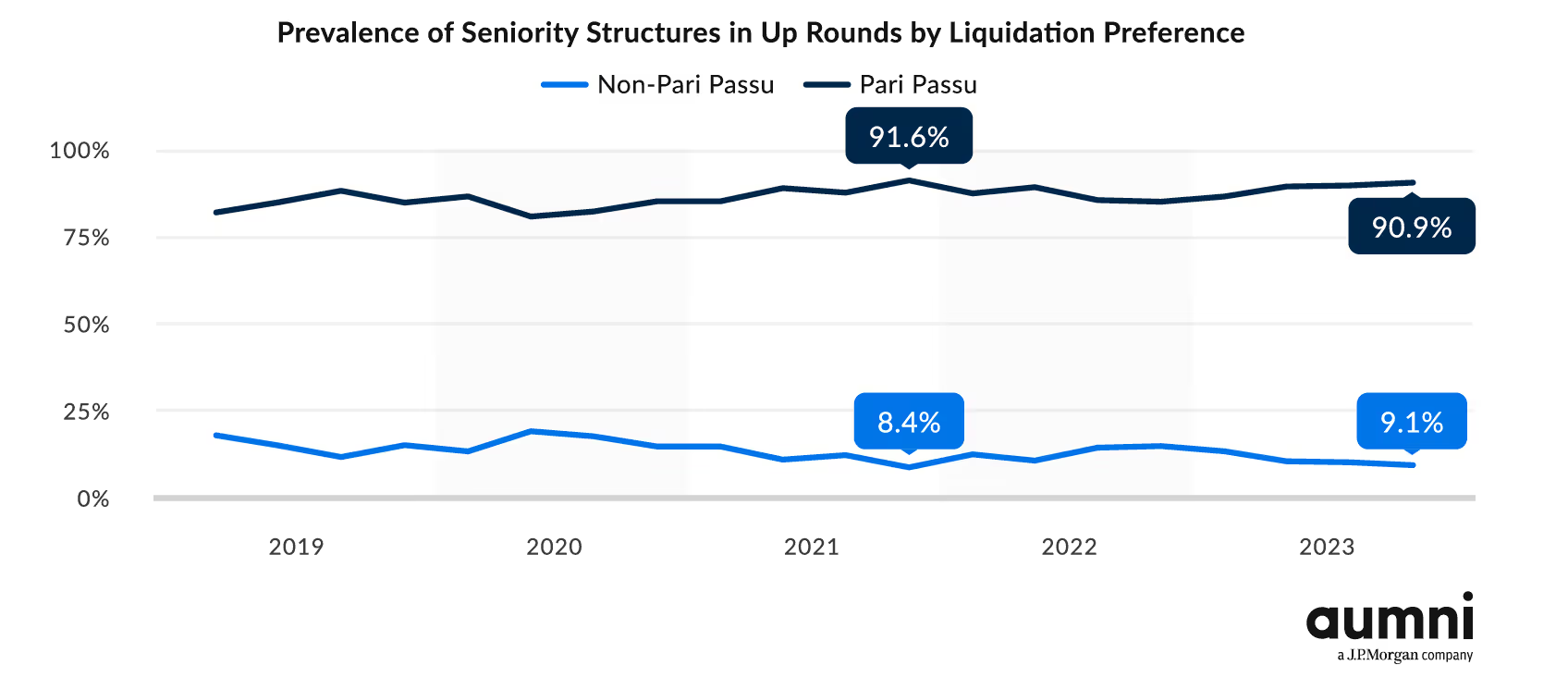

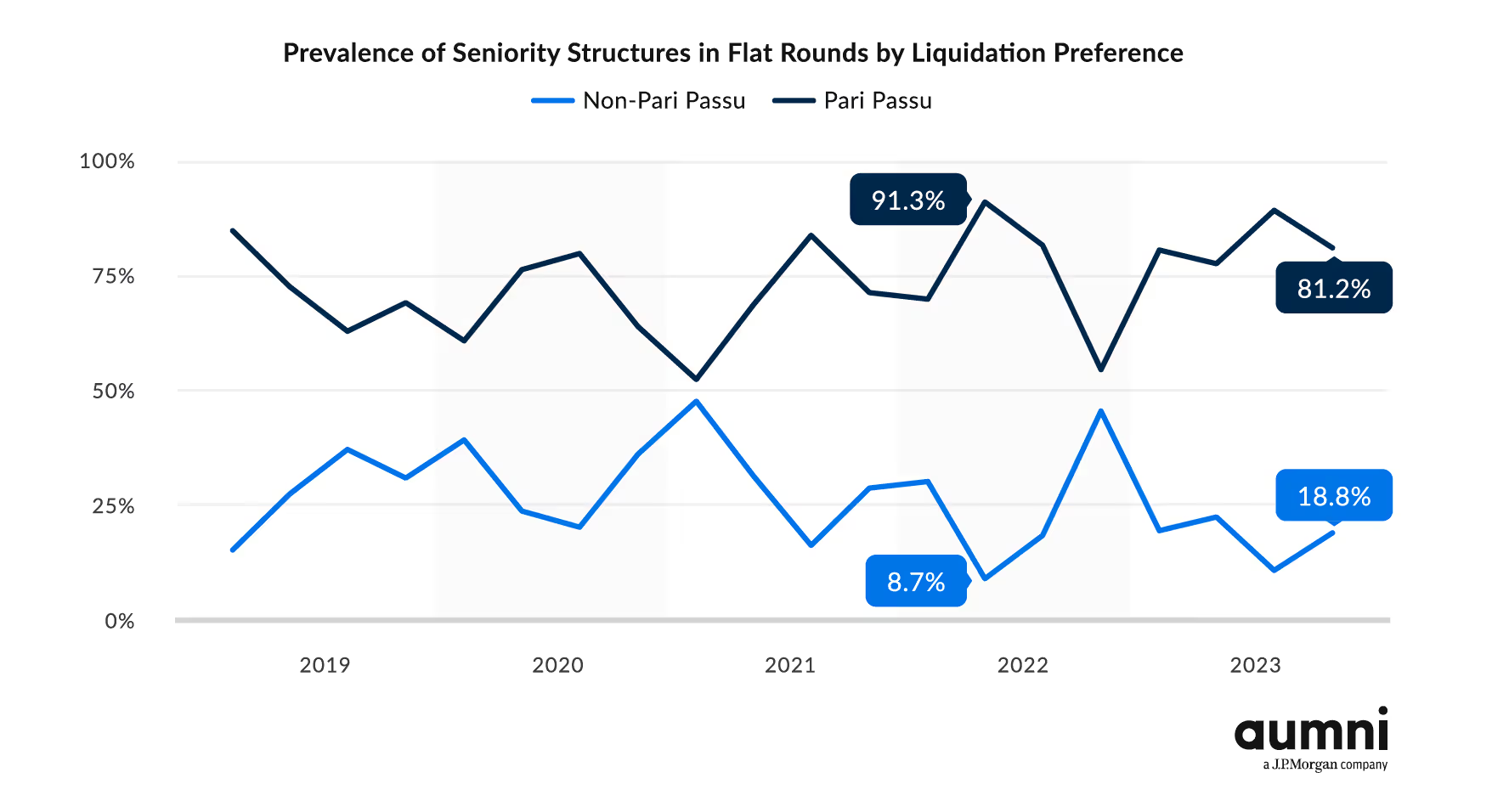

A closer examination, below, reveals that – perhaps unsurprisingly – the trend of more non-pari passu structure was largely driven by financings that were either flat or down rounds. While the percentage of up-round transactions that introduced seniority has remained relatively the same, both flat and down rounds saw meaningful shifts in deal structure throughout 2022, when nearly half of the transactions saw non-pari passu structure. Although trends normalized somewhat in 2023, the percentage of transactions with pari-passu structure was still below 2022 levels.

These deal term preferences, especially within late stage, imply an environment that continues to be investor-friendly, though with some easing in investor protection measures throughout 2023. Even still, the fluctuations in seniority structures indicate a market that is still finding its footing.

Aumni will continue monitoring these trends and other market conditions.

See more in the Aumni Venture Beacon Year End 2023 report.

Want to be the first to get these insights? Scroll down to sign up for our Venture Insights newsletter.

Photo by Bernd Dittrich on Unsplash

©2025 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC.

This material is not the product of J.P. Morgan’s Research Department. It is not a research report and is not intended as such. This material is provided for informational purposes only and is subject to change without notice. It is not intended as research, a recommendation, advice, offer or solicitation to buy or sell any financial product or service, or to be used in any way for evaluating the merits of participating in any transaction. Please consult your own advisors regarding legal, tax, accounting or any other aspects including suitability implications, for your particular circumstances or transactions. J.P. Morgan and its third-party suppliers disclaim any responsibility or liability whatsoever for the quality, fitness for a particular purpose, non-infringement, accuracy, currency or completeness of the information herein, and for any reliance on, or use of this material in any way. Any information or analysis in this material purporting to convey, summarize, or otherwise rely on data may be based on a sample or normalized set thereof. This material is provided on a confidential basis and may not be reproduced, redistributed or transmitted, in whole or in part, without the prior written consent of J.P. Morgan. Any unauthorized use is strictly prohibited. Any product names, company names and logos mentioned or included herein are trademarks or registered trademarks of their respective owners.

Aumni, Inc. (“Aumni”) is a wholly-owned subsidiary of JPMorgan Chase & Co. Access to the Aumni platform is subject to execution of an applicable platform agreement and order form and access will be granted by J.P. Morgan in its sole discretion. J.P. Morgan is the global brand name for JPMorgan Chase & Co. and its subsidiaries and affiliates worldwide. Aumni does not provide any accounting, regulatory, tax, insurance, investment, or legal advice. The recipient of any information provided by Aumni must make an independent assessment of any legal, credit, tax, insurance, regulatory and accounting issues with its own professional advisors in the context of its particular circumstances. Aumni is neither a broker-dealer nor a member of any exchanges or self-regulatory organizations.

383 Madison Ave, New York, NY 10017