A look into DPI, RVPI, TVPI, and IRR: Key metrics for evaluating VC fund performance

When evaluating venture capital (VC) fund performance, four metrics take center stage: Distributed to Paid-In (DPI), Residual Value to Paid-In (RVPI), Total Value to Paid-In (TVPI), and Internal Rate of Return (IRR). Together, these metrics provide LPs and GPs with a comprehensive view of both realized and unrealized returns, essential for assessing a fund’s overall performance.

A key aspect of this evaluation is understanding the distinction between net and gross performance metrics. Gross metrics reflect the fund’s performance before fees, expenses, and carried interest, providing insight into the fund’s raw returns. Conversely, net metrics account for these deductions, offering a more accurate representation of the actual returns received by investors.

By understanding these metrics and their implications, stakeholders can make informed investment decisions and accurately evaluate a fund’s success, setting the stage for deeper insights into each metric’s role in the valuation process.

Let’s break it down.

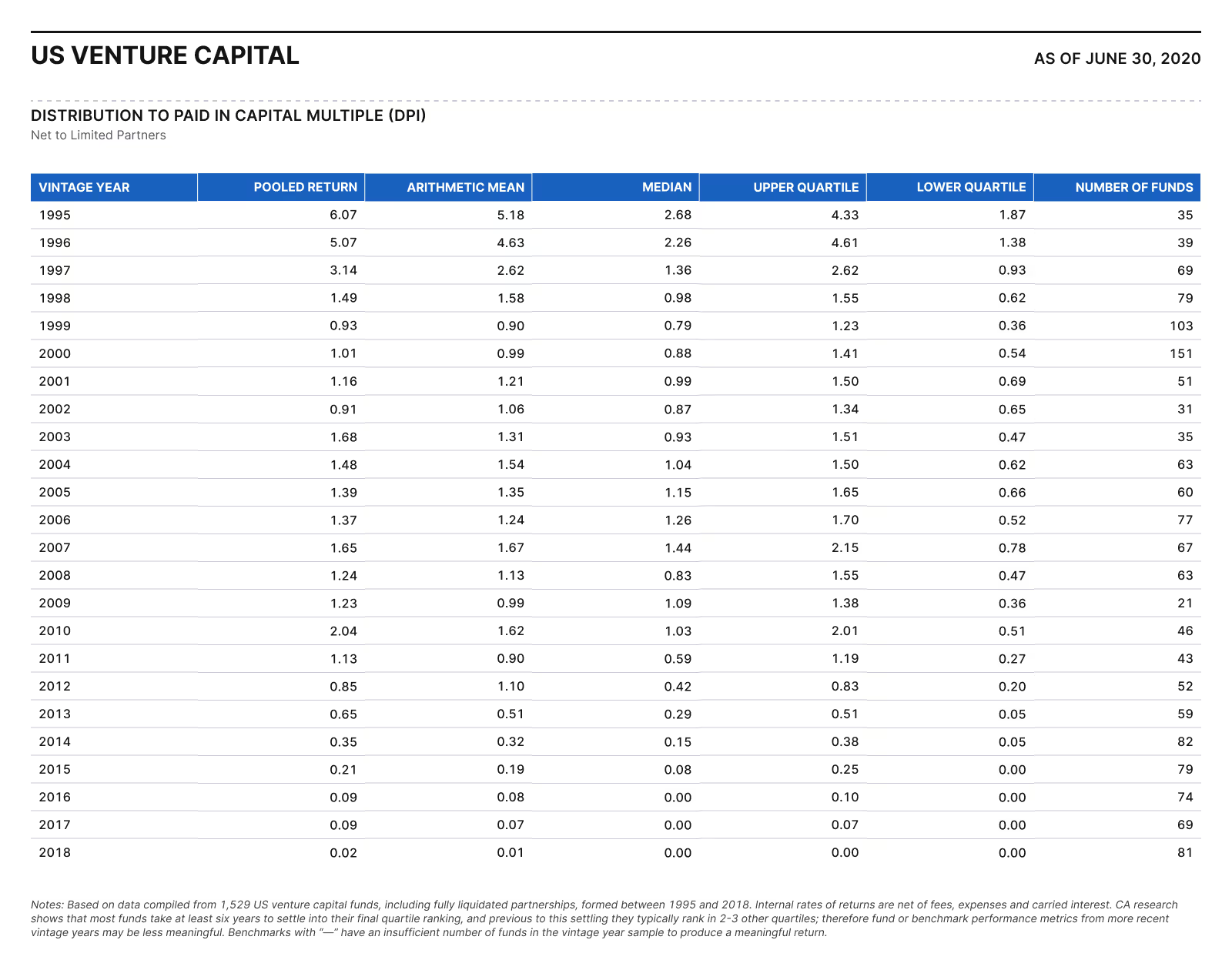

Distributed to Paid-In (DPI)

DPI is the realized return multiple, measuring how much capital has actually been paid back to LPs relative to what they invested.

DPI is an important metric for LPs because it shows tangible results—actual cash returned. It answers: “How much money have we gotten back so far?”

For example, a DPI of 1.0x means the fund has returned 100% of the capital called from LPs (i.e., LPs have gotten back an amount equal to their investment—breakeven). A DPI of 2.0x would mean the fund has doubled the investors’ money in actual distributions.

See below for venture capital DPIs from 1995 to 2018 according to Cambridge Associates US Venture Capital Index and Selected Benchmark Statistics.

Why DPI matters

Unlike IRR or TVPI, there’s no estimation or time value component. It’s a straightforward measure of payoff. A high DPI typically indicates a fund has been successful in delivering exits and returning capital.

It also helps gauge a fund’s liquidity. A fund might have a great TVPI on paper, but if DPI is low, it means most of the value is still tied up in the portfolio.

Many LPs pay attention to DPI because, ultimately, cash returned is what matters for their own liquidity and investment recycling.

Residual Value to Paid-In Capital (RVPI)

RVPI measures the value of a fund’s unrealized investments relative to the capital invested. It provides insight into the potential future returns that have yet to be realized. RVPI is crucial for understanding the current value of a fund’s portfolio and its potential to generate additional returns.

RVPI = Residual Value (fair value of the fund’s unrealized investments) / Paid-In Capital

See below for venture capital RVPIs from 1995 to 2018 according to Cambridge Associates US Venture Capital Index and Selected Benchmark Statistics.

Why RVPI matters

RVPI is important because it highlights the unrealized portion of a fund’s value, offering a glimpse into the potential future realizations. It complements DPI by providing a complete picture of both realized and unrealized returns.

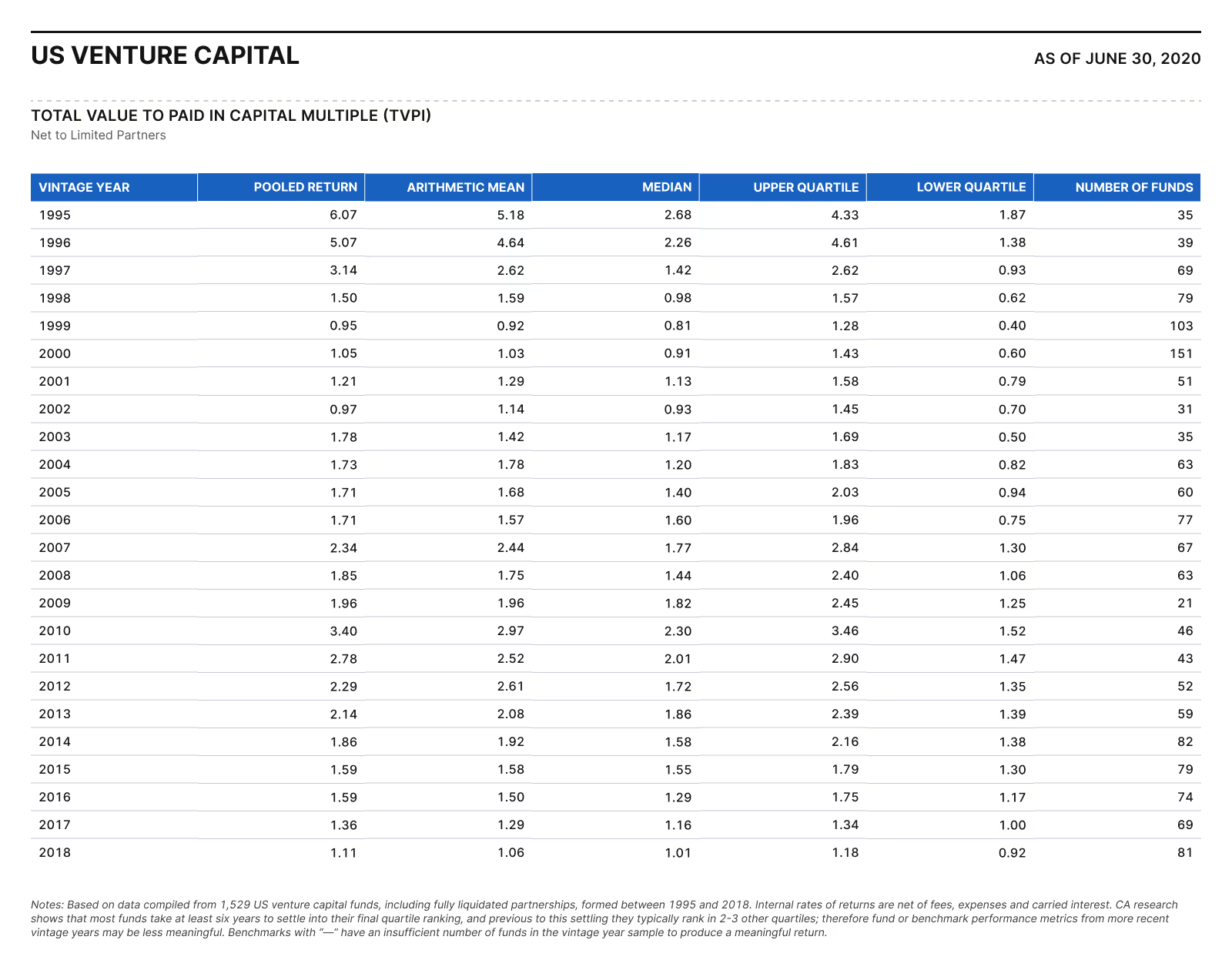

Total Value to Paid-In (TVPI)

TVPI measures the total value generated by the fund relative to the invested capital. It reflects both realized returns (actual cash distributed) and unrealized returns (current value of investments yet to be liquidated).

Mathematically: TVPI = (Distributed Value + Residual Value) / Paid-In Capital

This simplifies to TVPI = DPI (realized distributions) + RVPI (unrealized residual value).

For example, if investors paid $10 million into a fund, received $5 million back in distributions, and the remaining investments have an estimated value of $10 million, then the total value is $15 million, and the TVPI would be 1.5x.

See below for venture capital TVPIs from 1995 to 2018 according to Cambridge Associates US Venture Capital Index and Selected Benchmark Statistics.

Why TVPI matters

TVPI helps give a snapshot of a fund’s performance by combining what’s been realized with what’s still in the portfolio. This is useful for understanding the total potential outcome of the fund at a given time.

LPs and GPs look at TVPI to gauge how much the fund could return in total over its life, assuming the remaining investments pan out.

However, it’s important to note that TVPI relies on the valuations of unrealized investments, which are estimates, meaning TVPI can fluctuate with market conditions or valuation judgments.

Internal Rate of Return (IRR)

IRR is the annualized return rate that a fund generates, factoring in the timing of cash flows. The timing of cash flows is key in IRR calculations, as it accounts for when capital is deployed and returned, impacting the overall return rate.

Technically, IRR is the compounded annual return rate that sets the net present value (NPV) of all contributions and distributions to zero.

Simply put, IRR answers: "What yearly growth rate is the fund achieving on the invested capital?"

See below for venture capital IRRs from 1995 to 2018 according to Cambridge Associates US Venture Capital Index and Selected Benchmark Statistics.

Why IRR matters

Investors use IRR because it provides a consistent rate-based measure, making comparisons straightforward across different asset classes or funds. A higher IRR typically indicates that the fund is rapidly increasing investors' capital, while a lower IRR suggests slower growth.

However, a high IRR alone doesn't guarantee strong realized returns. The real measure of success includes how much cash investors actually receive. For a meaningful evaluation, IRR is considered alongside multiples like TVPI and DPI.

Using DPI, RVPI, TVPI, and IRR together

No single metric provides a complete picture of fund performance. Effective evaluation of fund performance involves viewing DPI, RVPI, TVPI, and IRR as complementary metrics:

- DPI reflects actual cash returned, crucial for assessing liquidity and realized success.

- RVPI highlights the unrealized portion of a fund’s value, indicating potential future returns and complementing DPI to provide a complete picture of both realized and unrealized returns.

- TVPI illustrates the overall value creation, combining both realized and unrealized returns.

- IRR shows the rate at which investor capital grows annually.

By understanding what each metric is saying—and what it isn’t— LPs, finance teams, and new VCs can more accurately evaluate a venture fund’s track record.

.avif)

.avif)

©2025 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC.

This material is not the product of J.P. Morgan’s Research Department. It is not a research report and is not intended as such. This material is provided for informational purposes only and is subject to change without notice. It is not intended as research, a recommendation, advice, offer or solicitation to buy or sell any financial product or service, or to be used in any way for evaluating the merits of participating in any transaction. Please consult your own advisors regarding legal, tax, accounting or any other aspects including suitability implications, for your particular circumstances or transactions. J.P. Morgan and its third-party suppliers disclaim any responsibility or liability whatsoever for the quality, fitness for a particular purpose, non-infringement, accuracy, currency or completeness of the information herein, and for any reliance on, or use of this material in any way. Any information or analysis in this material purporting to convey, summarize, or otherwise rely on data may be based on a sample or normalized set thereof. This material is provided on a confidential basis and may not be reproduced, redistributed or transmitted, in whole or in part, without the prior written consent of J.P. Morgan. Any unauthorized use is strictly prohibited. Any product names, company names and logos mentioned or included herein are trademarks or registered trademarks of their respective owners.

Aumni, Inc. (“Aumni”) is a wholly-owned subsidiary of JPMorgan Chase & Co. Access to the Aumni platform is subject to execution of an applicable platform agreement and order form and access will be granted by J.P. Morgan in its sole discretion. J.P. Morgan is the global brand name for JPMorgan Chase & Co. and its subsidiaries and affiliates worldwide. Aumni does not provide any accounting, regulatory, tax, insurance, investment, or legal advice. The recipient of any information provided by Aumni must make an independent assessment of any legal, credit, tax, insurance, regulatory and accounting issues with its own professional advisors in the context of its particular circumstances. Aumni is neither a broker-dealer nor a member of any exchanges or self-regulatory organizations.

383 Madison Ave, New York, NY 10017